Introduction

The credit derivative asset class covers single-name credit default swaps, index CDS, and total return swaps referencing debt instruments. Of the five asset classes in this series, credit shares the most structural similarity with equity — both group exposures by reference entity and use the same correlation-weighted Hedging Set Amount formula — but credit introduces an additional dimension that equity does not have: credit quality.

Where equity differentiates only between single-name and index, credit differentiates along two axes simultaneously: single-name versus index, and investment grade versus speculative grade (with a further sub-speculative grade tier for single names). This produces a more granular Supervisory Factor table than any other asset class in this series.

This article works through the credit asset class with the same depth as the previous four — Adjusted Notional, Supervisory Delta, Maturity Factor, Supervisory Factor — before showing how reference entity grouping and the correlation formula combine to produce the Hedging Set Amount. As with the other asset class articles, the PFE Multiplier and final aggregation are covered later in this series.

Single-Name vs Index vs Credit Quality — Three Dimensions

A single-name credit default swap references one specific corporate or sovereign borrower. An index credit default swap — such as a CDX or iTraxx index — references a standardised basket of borrowers. This single-name/index distinction mirrors equity exactly.

What credit adds is a credit quality dimension. Single-name credit exposures are split into three tiers: investment grade, speculative grade, and sub-speculative grade. Index exposures are split into only two tiers: investment grade and speculative grade. This reflects the reality that default risk — unlike general market risk — varies enormously and non-linearly with credit quality, in a way that justifies a much finer Supervisory Factor table than equity’s simple single-name/index split.

What Defines a Credit Hedging Set

Under §217.132(c)(2)(iii)(C), the hedging set definition for credit derivatives mirrors equity in its breadth:

“With respect to credit derivative contract, all such contracts within a netting set.”

All credit derivative contracts within a netting set form a single hedging set, regardless of how many distinct reference entities or credit quality tiers are involved. As with equity, the differentiation happens inside the Hedging Set Amount formula through reference-entity grouping, not through separate hedging sets.

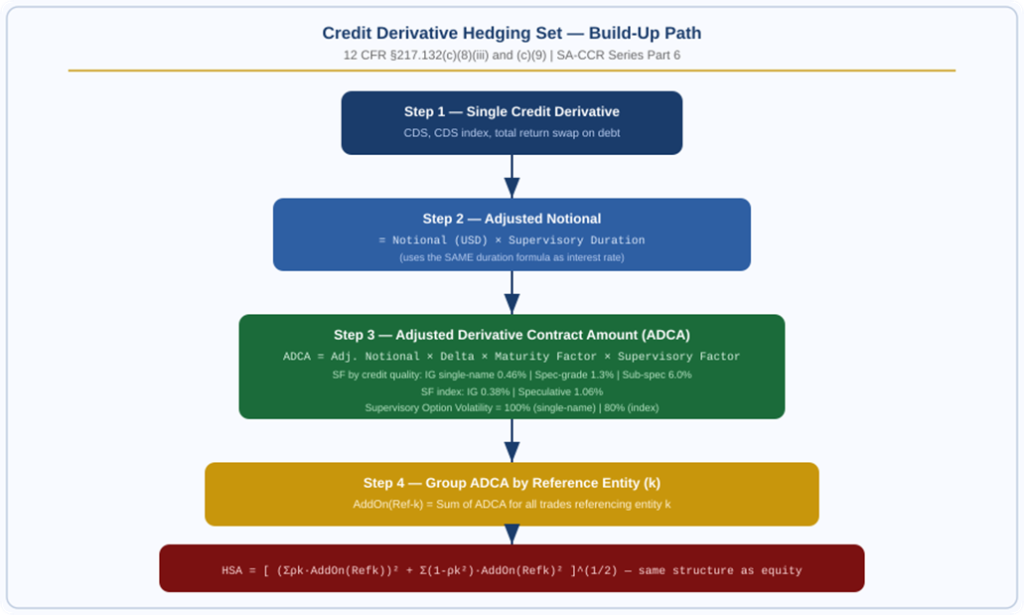

Step 1 — Calculate the Adjusted Notional

Credit derivatives are one of only two asset classes in this series (alongside interest rate) that require the Supervisory Duration calculation, because credit default swaps reference a protection period with a defined start and end date, just like an interest rate swap references a payment schedule.

| SD = [ e^(−0.05 × S/250) − e^(−0.05 × E/250) ] / 0.05 |

| S = business days from today until the contract’s start date (0 if already started) | E = business days from today until the contract’s end date | Floor: SD ≥ 0.04 |

| Adjusted Notional = Notional (in USD) × Supervisory Duration |

| Identical formula structure to interest rate. Notional must be converted to USD using the exchange rate on the calculation date if denominated in another currency. |

| Worked Example 1 — 5-Year Single-Name CDS Trade: $30,000,000 notional, bank buys protection (long protection) Start date: today (S = 0 business days) End date: 5 years from today (E = 1,250 business days, approx.) SD = [e^(-0.05×0/250) – e^(-0.05×1250/250)] / 0.05 SD = [1.0000 – 0.7788] / 0.05 = 4.424 (identical calculation method to the interest rate example in Part 3 of this series, since the formula is the same) Adjusted Notional = $30,000,000 × 4.424 = $132,720,000 |

Step 2 — Determine the Supervisory Delta

For Linear Instruments (CDS, Index CDS)

Buying credit protection (the bank gains if the reference entity’s credit quality deteriorates or it defaults) and selling credit protection (the bank gains if credit quality improves or stays stable) are treated as opposite directions:

| Delta = +1 (sold protection — long credit risk) or −1 (bought protection — short credit risk) |

| Sold protection behaves like a long credit position: value falls if the reference entity’s credit quality worsens. |

For Credit Options and CDS with Embedded Optionality

Credit derivatives with option-like payoffs use the same Black-Scholes-style delta structure as the other asset classes, with credit-specific supervisory option volatility:

| Delta = Φ( [ln(P/K) + 0.5σ²T/250] / (σ√(T/250)) ) |

| Φ = standard normal CDF | P, K reference the relevant credit spread or price | T = business days to exercise | σ = supervisory option volatility |

| Category | Supervisory Option Volatility |

| Credit, single name | 100% |

| Credit, index | 80% |

Step 3 — Calculate the Maturity Factor

As with every other asset class in this series, the Maturity Factor formula structure is identical.

For Trades Subject to a Variation Margin Agreement

| MF = (3/2) × √(MPOR / 250) |

| Same MPOR floors apply across all asset classes: 10 business days standard, 5 for client-facing trades, 20 for large or illiquid netting sets. |

For Trades Not Subject to a Variation Margin Agreement

| MF = √( min{M, 250} / 250 ) |

| M = remaining maturity in business days, floored at 10 business days |

Step 4 — The Supervisory Factor for Credit

This is where the credit asset class becomes the most granular in the entire SA-CCR framework. Table 3 to §217.132 sets out five distinct categories:

| Category | Credit Quality | Supervisory Factor | Correlation Factor (ρ) |

| Credit, single name | Investment grade | 0.46% | 50% |

| Credit, single name | Speculative grade | 1.3% | 50% |

| Credit, single name | Sub-speculative grade | 6.0% | 50% |

| Credit, index | Investment grade | 0.38% | 80% |

| Credit, index | Speculative grade | 1.06% | 80% |

The progression from 0.46% (single-name investment grade) to 6.0% (single-name sub-speculative grade) — a more than 13-fold increase — reflects how dramatically default risk accelerates as credit quality deteriorates. Note that the correlation factor ρ does not vary by credit quality within a category — it is 50% for all single-name credit regardless of rating, and 80% for all index credit regardless of rating. Only the Supervisory Factor captures the credit quality dimension; ρ captures only the single-name/index dimension.

Putting It Together — The ADCA Formula

| ADCA = Adjusted Notional × Supervisory Delta × Maturity Factor × Supervisory Factor |

| Worked Example 2 — Full ADCA Calculation (Single-Name, Speculative Grade) Trade: $30,000,000 CDS, bank sold protection (from Example 1) Reference entity credit quality: Speculative grade Subject to a daily variation margin agreement Adjusted Notional (from Example 1): $132,720,000 Supervisory Delta (sold protection, long credit): +1 MPOR: 10 business days (standard, daily VM) Maturity Factor = 1.5 × √(10/250) = 1.5 × 0.2 = 0.300 Supervisory Factor (single-name, speculative grade): 1.3% ADCA = 132,720,000 × 1 × 0.300 × 0.013 ADCA = $517,608 |

| Worked Example 3 — Same Trade, Investment Grade Instead Identical trade terms, but reference entity is investment grade Supervisory Factor (single-name, investment grade): 0.46% ADCA = 132,720,000 × 1 × 0.300 × 0.0046 ADCA = $183,153 The investment-grade version of this trade produces an ADCA roughly 65% lower than the speculative-grade version, purely from the Supervisory Factor difference (0.46% vs 1.3%) — this is the single largest driver of ADCA variation within credit. |

Figure 1: Credit derivative hedging set build-up — credit quality drives the Supervisory Factor | Source: 12 CFR §217.132(c)(8)(iii), (c)(9)

Step 5 — Grouping by Reference Entity

Exactly as with equity, every credit derivative trade’s ADCA is allocated to its reference entity — the specific borrower (for single-name CDS) or the specific index (for index CDS) — and summed within that grouping:

| AddOn(Ref_k) = Σ ADCA for all trades referencing entity k |

| k indexes each distinct reference entity. A bank with CDS protection bought and sold on the same borrower, plus an index position, would have multiple values of k within one hedging set. |

Critically, credit quality does not create a separate grouping dimension here — it only affects the Supervisory Factor used when calculating each trade’s ADCA in Step 3. Once ADCA is calculated, grouping happens purely by reference entity identity, combining trades of potentially different credit quality tiers on the same borrower (though in practice, a single borrower typically has one rating at a time).

Step 6 — Calculating the Hedging Set Amount

The credit asset class uses the identical Hedging Set Amount formula structure as equity:

| HSA = [ (Σρk × AddOn(Refk))² + Σ(1−ρk²) × (AddOn(Refk))² ]^(1/2) |

| ρk = 50% for single-name reference entities, 80% for index reference entities. Summations run over all k reference entities in the hedging set. |

The economic interpretation is the same as equity: the first term captures the systematic credit risk component shared across reference entities (broad credit cycle, sector-wide spread widening), and the second term captures the idiosyncratic component specific to each individual borrower (company-specific default risk, covenant breaches, single-name credit events).

| Worked Example 4 — Hedging Set Amount with Mixed Credit Exposures Hedging set contains three reference entities: Entity 1 (single-name, speculative): AddOn = $517,608 ρ = 0.50 Entity 2 (single-name, investment): AddOn = $183,153 ρ = 0.50 Entity 3 (CDX index, investment): AddOn = $610,000 ρ = 0.80 Systematic term: Σρk·AddOn(Refk) = (0.50×517,608)+(0.50×183,153)+(0.80×610,000) = 258,804 + 91,577 + 488,000 = $838,381 Squared: (838,381)² ≈ 7.0288E11 Idiosyncratic term: Entity 1: (1-0.25)×(517,608)² = 0.75×2.6791E11 = 2.0093E11 Entity 2: (1-0.25)×(183,153)² = 0.75×3.3545E10 = 2.5159E10 Entity 3: (1-0.64)×(610,000)² = 0.36×3.7210E11 = 1.3396E11 Sum ≈ 3.6004E11 HSA = [7.0288E11 + 3.6004E11]^(1/2) = [1.0629E12]^(1/2) HSA ≈ $1,031,000 Compare to a simple sum of AddOns (517,608+183,153+610,000 = $1,310,761) — diversification across distinct reference entities again reduces the recognised exposure meaningfully. |

Special Cases Within the Credit Asset Class

Purchased Credit Protection Not Treated as Counterparty Credit Risk

A bank that purchases a credit derivative recognised under §217.134 or §217.135 as a credit risk mitigant for an exposure that is not a covered position under Subpart F is not required to calculate a separate counterparty credit risk capital requirement for that credit derivative, provided it applies this treatment consistently and either includes or excludes all such credit derivatives subject to a master netting agreement from its counterparty credit risk measures.

Protection Sellers Treat the Position as a Wholesale Exposure

A bank that is the protection provider in a credit derivative must treat the position as a wholesale exposure to the reference obligor — not as a derivative subject to standard counterparty credit risk capital — again provided this treatment is applied consistently, unless the bank treats the credit derivative as a covered position under Subpart F, in which case a supplemental counterparty credit risk capital requirement still applies.

First-to-Default and Subsequent-to-Default Baskets

For first-to-default credit derivatives, there are no underlying exposures subordinated to the bank’s exposure. For second-or-subsequent-to-default credit derivatives, the smallest (n−1) notional amounts of the underlying exposures are treated as subordinated — this affects the attachment and detachment point calculation used in the supervisory delta formula for CDO-tranche-style credit derivatives.

Quick Summary

- All credit derivative contracts within a netting set form a single hedging set — there is no split by currency, currency pair, or credit quality tier at the hedging-set level.

- Credit is one of only two asset classes (with interest rate) that requires the Supervisory Duration calculation for Adjusted Notional.

- The Supervisory Factor table for credit is the most granular of any asset class: 0.46% to 6.0% for single-name (by credit quality), and 0.38% to 1.06% for index.

- The correlation factor ρ depends only on single-name vs index (50% vs 80%) — not on credit quality.

- ADCAs are grouped by reference entity (the specific borrower or index), exactly as with equity.

- The Hedging Set Amount formula is structurally identical to equity: a systematic term using ρ-weighted sums, plus an idiosyncratic term using (1−ρ²)-weighted squared AddOns.

- Credit quality has a dramatically larger effect on ADCA than any other variable in the formula — moving from investment grade to speculative grade alone can change ADCA by a factor of nearly 3x, and to sub-speculative grade by over 13x.

Frequently Asked Questions

Why does credit have three credit quality tiers for single-name but only two for index?

Index products are diversified baskets that, by construction, blend multiple borrowers’ credit risk together — extreme tail scenarios for any single borrower in the index are diluted by the other constituents. A standardised credit index like CDX or iTraxx is generally constructed from either investment grade or speculative grade names, with no widely-traded sub-speculative grade index equivalent. Single-name CDS, by contrast, can reference borrowers across the full credit spectrum, including deeply distressed sub-speculative grade names, justifying the additional third tier.

Does the Supervisory Factor or the correlation factor change more credit risk sensitivity?

The Supervisory Factor has by far the larger effect, since it varies by a factor of more than 13x across credit quality tiers (0.46% to 6.0%) for single-name credit. The correlation factor ρ only takes two possible values (50% or 80%) and only varies based on single-name versus index status, not credit quality — its effect on the final Hedging Set Amount is comparatively modest next to the Supervisory Factor’s direct multiplicative impact on each trade’s ADCA.

Why is the Adjusted Notional formula for credit identical to interest rate?

Both asset classes reference instruments with a defined time horizon — a credit default swap has a protection period with a start and end date, just as an interest rate swap has a payment schedule with a start and end date. The Supervisory Duration formula captures the time-weighted sensitivity of the contract’s cash flows in both cases, which is why the regulation applies the identical formula structure to both asset classes.

Can the same reference entity appear with different credit quality tiers within one hedging set?

In principle, the regulation groups ADCA by reference entity identity (k), not by credit quality tier. In practice, a single borrower has one prevailing credit rating at any point in time, so this scenario would typically only arise from a rating change between the inception of different trades referencing the same borrower, or from differing internal versus external rating assessments used for different transactions.