Introduction

The equity asset class covers single stock derivatives, equity index derivatives, equity options, and equity total return swaps. Structurally, it sits between interest rate and exchange rate in complexity: like FX, there are no maturity time buckets; like credit, there is a correlation structure that distinguishes single-name exposures from index exposures.

This article works through the equity asset class with the same granularity as the previous two articles in this series — Adjusted Notional, Supervisory Delta, Maturity Factor, and Supervisory Factor — before showing exactly how individual trade ADCAs are grouped by reference entity and combined into a Hedging Set Amount using the reference-entity correlation formula.

As with the IR and FX articles, this piece stops at the Hedging Set Amount. The PFE Multiplier and full cross-asset-class aggregation into total PFE are covered later in this series.

Single-Name vs Index — The Core Distinction

The defining feature of the equity asset class (shared with credit derivatives) is the split between single-name exposures and index exposures. A single-name equity derivative references one specific company’s stock. An index equity derivative — for example, a total return swap on the S&P 500 — references a basket of underlying names.

This distinction matters because index positions are inherently more diversified than single-name positions. The regulation reflects this directly in two places: the Supervisory Factor (lower for index than single-name) and the Supervisory Correlation Factor used when combining exposures across different reference entities within a hedging set.

What Defines an Equity Hedging Set

Under §217.132(c)(2)(iii)(D), the hedging set definition for equity derivatives is broad:

“With respect to equity derivative contracts, all such contracts within a netting set.”

Unlike interest rate (split by currency) or exchange rate (split by currency pair), all equity derivative contracts within a single netting set form one hedging set, regardless of how many different underlying companies or indices are referenced. The differentiation between reference entities happens inside the hedging set amount formula itself, not through separate hedging sets.

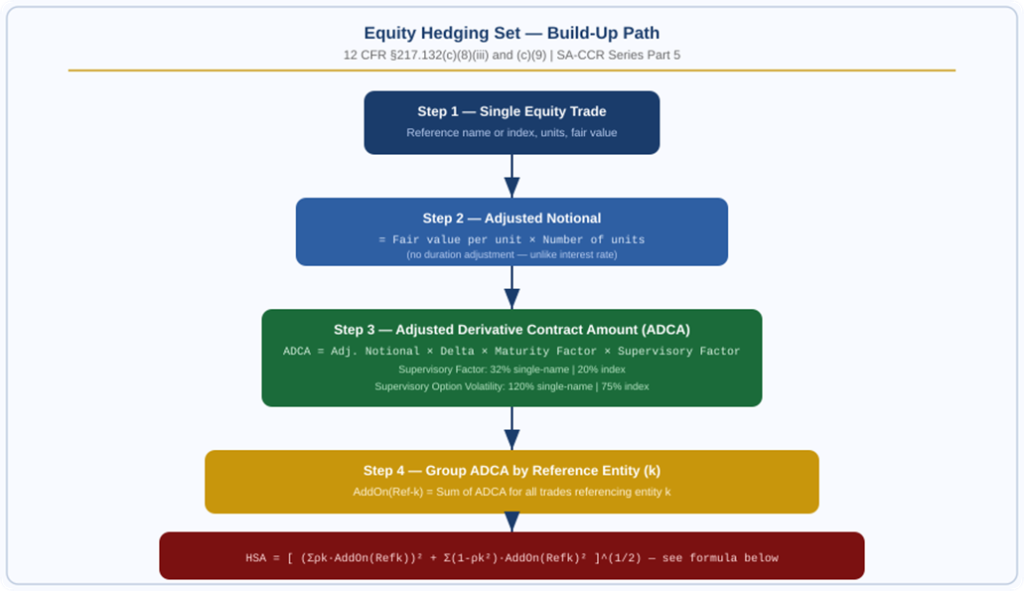

Step 1 — Calculate the Adjusted Notional

Equity derivatives do not require a Supervisory Duration calculation the way interest rate trades do. The Adjusted Notional is simply the current market value of the position:

| Adjusted Notional = Fair Value of One Unit × Number of Units Referenced |

| For a single stock future: current share price × number of shares under the contract. For an index swap: index level × multiplier × number of contracts. |

| Worked Example 1 — Single-Name Equity Total Return Swap Trade: Total return swap on 100,000 shares of a single company Current share price: $145.00 Adjusted Notional = 145.00 × 100,000 Adjusted Notional = $14,500,000 |

| Worked Example 2 — Index Equity Future Trade: Index future, 50 contracts, index multiplier $50 per point Current index level: 4,850 Adjusted Notional = 4,850 × 50 × 50 Adjusted Notional = $12,125,000 |

Volatility Derivative Variant

For an equity derivative that is a volatility derivative — for example, a variance swap on a single stock or index — the unit price in the Adjusted Notional formula is replaced with the underlying volatility referenced by the contract, and the number of units is replaced with the notional amount of the volatility derivative itself.

Step 2 — Determine the Supervisory Delta

For Linear Instruments (Futures, Total Return Swaps)

| Delta = +1 (long the equity) or −1 (short the equity) |

| Determined by whether the contract’s value rises or falls when the reference equity price increases. |

For Equity Options

Equity options use the same Black-Scholes-style delta structure as interest rate and FX options, with equity-specific supervisory option volatility:

| Delta = Φ( [ln(P/K) + 0.5σ²T/250] / (σ√(T/250)) ) |

| Φ = standard normal CDF | P = current equity price/level | K = strike | T = business days to exercise | σ = supervisory option volatility |

The supervisory option volatility differs sharply between single-name and index equity, reflecting the greater idiosyncratic volatility of individual stocks compared to diversified baskets:

| Category | Supervisory Option Volatility |

| Equity, single name | 120% |

| Equity, index | 75% |

Step 3 — Calculate the Maturity Factor

The Maturity Factor formula is identical in structure across all asset classes covered in this series so far.

For Trades Subject to a Variation Margin Agreement

| MF = (3/2) × √(MPOR / 250) |

| Same MPOR floors as IR and FX: minimum 10 business days standard, 5 for client-facing trades, 20 for large or illiquid netting sets. |

For Trades Not Subject to a Variation Margin Agreement

| MF = √( min{M, 250} / 250 ) |

| M = remaining maturity in business days, floored at 10 business days |

Step 4 — The Supervisory Factor for Equity

Equity is the first asset class in this series where the Supervisory Factor varies based on the nature of the exposure rather than being a single flat number:

| Category | Supervisory Factor | Supervisory Correlation Factor (ρ) |

| Equity, single name | 32% | 50% |

| Equity, index | 20% | 80% |

Single-name equity carries a substantially higher Supervisory Factor (32%) than index equity (20%), reflecting the additional idiosyncratic risk of an individual company versus a diversified basket. The correlation factor ρ — used in Step 5 below — works in the opposite direction: index exposures have a higher correlation factor (80% vs 50%) because the underlying constituents of a major index are, by construction, more correlated with the broad market factor than any single stock is.

Putting It Together — The ADCA Formula

| ADCA = Adjusted Notional × Supervisory Delta × Maturity Factor × Supervisory Factor |

| Worked Example 3 — Full ADCA Calculation (Single-Name) Trade: Total return swap, long 100,000 shares (from Example 1) Maturity: 18 months, not subject to a variation margin agreement Adjusted Notional (from Example 1): $14,500,000 Supervisory Delta (long the equity): +1 Maturity Factor: M = 18 months ≈ 375 business days MF = √(min(375,250)/250) = √(250/250) = √1 = 1.000 (floored at the 250-day cap, since M exceeds 1 year) Supervisory Factor (single-name equity): 32% ADCA = 14,500,000 × 1 × 1.000 × 0.32 ADCA = $4,640,000 |

Figure 1: Equity hedging set build-up — grouped by reference entity, correlated using ρ | Source: 12 CFR §217.132(c)(8)(iii), (c)(9)

Step 5 — Grouping by Reference Entity

Before the Hedging Set Amount can be calculated, every trade’s ADCA must be allocated to its reference entity — the specific company (for single-name trades) or the specific index (for index trades) that the contract references. All ADCAs referencing the same entity are summed:

| AddOn(Ref_k) = Σ ADCA for all trades referencing entity k |

| k indexes each distinct reference entity within the hedging set — for example, three different single-name stocks plus one index would give four values of k. |

This grouping step is what distinguishes equity (and credit) from interest rate and FX. Rather than time buckets, the organizing principle here is identity of the underlying reference entity.

Step 6 — Calculating the Hedging Set Amount

With AddOn(Ref_k) calculated for every reference entity k in the hedging set, the Hedging Set Amount combines them using a correlation-weighted formula:

| HSA = [ (Σρk × AddOn(Refk))² + Σ(1−ρk²) × (AddOn(Refk))² ]^(1/2) |

| ρk = supervisory correlation factor for reference entity k (50% single-name, 80% index). Summations run over all k reference entities in the hedging set. |

This formula has two parts. The first term — the squared sum of ρk-weighted AddOns — captures the systematic, correlated component of risk across all reference entities (think of this as the portion of each stock’s movement explained by the broad market factor). The second term — the sum of (1−ρk²)-weighted squared AddOns — captures the idiosyncratic, uncorrelated component specific to each individual name.

The structure means a hedging set containing several single-name exposures across genuinely different companies gets meaningful diversification credit through the idiosyncratic term, while still recognising that all equities share some common exposure to the broad market through the systematic term.

| Worked Example 4 — Hedging Set Amount with Mixed Exposures Hedging set contains three reference entities: Entity 1 (single-name stock A): AddOn = $4,640,000 ρ = 0.50 Entity 2 (single-name stock B): AddOn = $2,100,000 ρ = 0.50 Entity 3 (equity index): AddOn = $3,800,000 ρ = 0.80 Systematic term: Σρk·AddOn(Refk) = (0.50×4,640,000)+(0.50×2,100,000)+(0.80×3,800,000) = 2,320,000 + 1,050,000 + 3,040,000 = $6,410,000 Squared: (6,410,000)² = 4.1088E13 Idiosyncratic term: Entity 1: (1-0.50²)×(4,640,000)² = 0.75×2.1530E13 = 1.6148E13 Entity 2: (1-0.50²)×(2,100,000)² = 0.75×4.4100E12 = 3.3075E12 Entity 3: (1-0.80²)×(3,800,000)² = 0.36×1.4440E13 = 5.1984E12 Sum = 2.4654E13 HSA = [4.1088E13 + 2.4654E13]^(1/2) = [6.5742E13]^(1/2) HSA ≈ $8,108,000 Compare to a simple sum of AddOns (4,640,000+2,100,000+3,800,000 = $10,540,000) — the correlation formula recognises meaningful diversification benefit across the three distinct reference entities. |

Special Cases Within the Equity Asset Class

Collateralized Debt Obligation Tranches Referencing Equity-Like Structures

Where an equity derivative contract is structured as a CDO tranche, the supervisory delta adjustment uses the specialised attachment/detachment point formula covered in Part 1 of this series, rather than the standard linear or option delta.

Volatility Derivatives

Equity volatility derivatives use the same hedging-set grouping and correlation structure as standard equity derivatives, but as noted in Step 1, the Adjusted Notional substitutes underlying volatility for unit price and the volatility derivative’s own notional for the number of units.

Equity Derivatives Treated as Covered Positions Under Subpart F

If a bank treats an equity derivative contract as a covered position under the market risk rules in Subpart F, it must still calculate a supplemental counterparty credit risk capital requirement under §217.132 in certain circumstances described in §217.155 — the equity derivative does not escape counterparty credit risk treatment simply because it is also subject to market risk capital.

Quick Summary

- All equity derivative contracts within a netting set form a single hedging set — there is no split by currency or currency pair as with interest rate or FX.

- Adjusted Notional for equity is simply fair value per unit × number of units — no duration adjustment is needed.

- The Supervisory Factor differs by category: 32% for single-name equity, 20% for index equity.

- Supervisory option volatility also differs: 120% for single-name, 75% for index — reflecting higher idiosyncratic volatility in individual stocks.

- ADCAs are grouped by reference entity (the specific company or index referenced) before aggregation, not by time bucket.

- The Hedging Set Amount formula splits risk into a systematic (correlated) component using ρ = 50% (single-name) or 80% (index), and an idiosyncratic component using (1−ρ²).

- This correlation structure gives genuine diversification credit for holding multiple distinct, uncorrelated single-name exposures within the same hedging set.

Frequently Asked Questions

Why is the Supervisory Factor higher for single-name equity than for index equity?

Single-name equity carries idiosyncratic risk specific to one company — earnings surprises, company-specific news, takeover risk — on top of broad market risk. An index, being a diversified basket, has much of that idiosyncratic risk averaged out, leaving primarily systematic market risk. The higher 32% factor for single-name versus 20% for index reflects this additional company-specific risk.

Why does the correlation factor ρ work in the opposite direction to the Supervisory Factor?

ρ measures how correlated a reference entity’s movements are with the broader systematic risk factor used in the Hedging Set Amount formula. An index, by construction, moves closely with the broad market (ρ = 80%). A single stock has a meaningful idiosyncratic component that is not explained by the broad market alone, so its correlation to the systematic factor is lower (ρ = 50%) even though its overall volatility (reflected in the Supervisory Factor) is higher.

How does grouping by reference entity differ from time bucketing in the interest rate asset class?

Interest rate trades are grouped by maturity because risk on the same yield curve is correlated across time. Equity trades are grouped by reference entity (company or index) because the risk driver is which specific equity is referenced, not when the contract matures. A 3-month and a 3-year total return swap on the same stock are grouped together under that one reference entity, regardless of their different maturities.

Does an equity hedging set ever split by currency the way FX does?

No. The hedging set definition in §217.132(c)(2)(iii)(D) includes all equity derivative contracts within a netting set, with no currency-based split. The currency in which an equity derivative is denominated does not create separate hedging sets the way it does for interest rate and FX.

Pingback: SA-CCR: PFE Multiplier and Exposure at Default