Introduction

The commodity asset class covers derivative contracts referencing energy products, metals, agricultural products, and other physical commodities. This is the final asset class in our seven-part series working through the SA-CCR Hedging Set Amount calculation for every asset class recognised under 12 CFR §217.132.

Structurally, commodity sits closest to equity: there is no time-bucketing as with interest rate, no currency-pair splitting as with FX, and the Adjusted Notional formula is identical to equity’s simple fair-value-times-units approach. What makes commodity distinctive is its four-category structure and a Hedging Set Amount formula that applies a single correlation factor across all categories simultaneously, rather than the per-reference-entity correlation used in equity and credit.

This article completes the Adjusted Derivative Contract Amount and Hedging Set Amount build-up for commodity. As with every asset-class article in this series, the PFE Multiplier and the final cross-asset-class aggregation into total PFE are covered in the concluding article of this broader Counterparty Credit Risk series.

The Four Commodity Categories

Under §217.132(c)(2)(iii)(E), commodity hedging sets are defined by reference to one of four specific categories:

“With respect to a commodity derivative contract, all such contracts within a netting set that reference one of the following commodity categories: Energy, metal, agricultural, or other commodities.”

This is a meaningfully different structure from equity and credit. Where equity and credit form one hedging set per netting set regardless of how many reference entities are involved, commodity forms one hedging set per category. A bank with crude oil swaps, gold forwards, and wheat futures against the same counterparty has three separate commodity hedging sets — energy, metal, and agricultural respectively — each calculated independently up to the Hedging Set Amount stage.

Within the energy category specifically, the regulation further distinguishes electricity from other energy products at the Supervisory Factor and volatility level, even though both remain within the single energy hedging set.

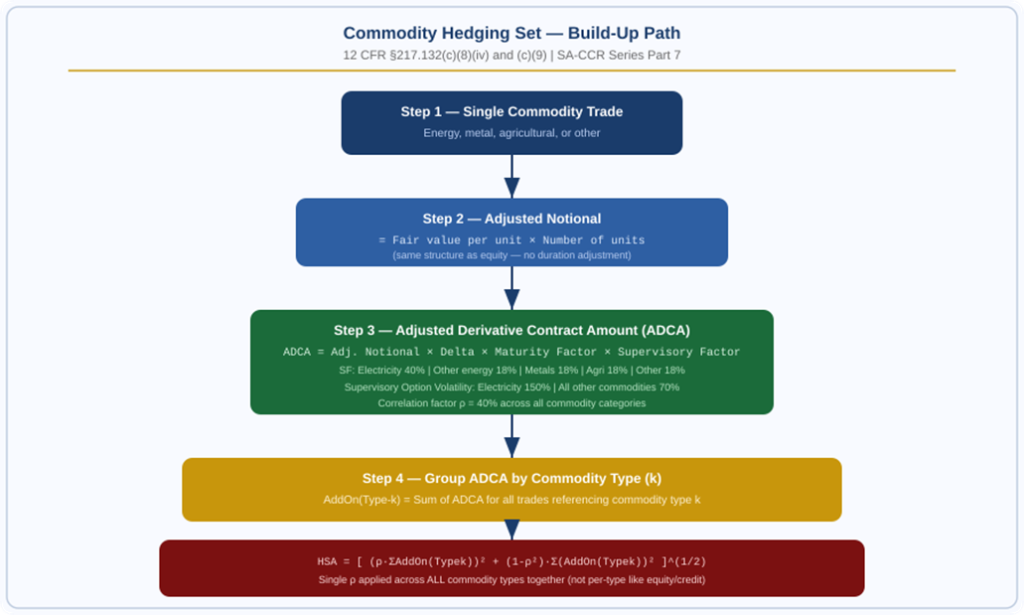

Step 1 — Calculate the Adjusted Notional

Like equity, commodity derivatives do not require a Supervisory Duration calculation. The Adjusted Notional is the current market value of the position, exactly as with equity:

| Adjusted Notional = Fair Value of One Unit × Number of Units Referenced |

| For a crude oil swap: current price per barrel × number of barrels. For a gold forward: current spot price per ounce × number of ounces. |

| Worked Example 1 — Crude Oil Swap (Energy Category) Trade: Swap on 100,000 barrels of WTI crude Current price: $78.50 per barrel Adjusted Notional = 78.50 × 100,000 Adjusted Notional = $7,850,000 |

| Worked Example 2 — Gold Forward (Metal Category) Trade: Forward on 5,000 troy ounces of gold Current spot price: $2,340 per ounce Adjusted Notional = 2,340 × 5,000 Adjusted Notional = $11,700,000 |

Step 2 — Determine the Supervisory Delta

For Linear Instruments (Forwards, Swaps, Futures)

| Delta = +1 (long the commodity) or −1 (short the commodity) |

| Determined by whether the contract’s value rises or falls when the reference commodity price increases. |

For Commodity Options

Commodity options use the same Black-Scholes-style delta structure as the other four asset classes:

| Delta = Φ( [ln(P/K) + 0.5σ²T/250] / (σ√(T/250)) ) |

| Φ = standard normal CDF | P = current commodity price | K = strike | T = business days to exercise | σ = supervisory option volatility |

| Commodity Category | Supervisory Option Volatility |

| Energy — Electricity | 150% |

| Energy — Other | 70% |

| Metals | 70% |

| Agricultural | 70% |

| Other commodities | 70% |

Electricity stands apart from every other commodity sub-category with a dramatically higher supervisory option volatility of 150% versus 70% for all others. This reflects the well-documented extreme price volatility of electricity markets, driven by the physical reality that electricity cannot be stored economically at scale and demand must be met in real time.

Step 3 — Calculate the Maturity Factor

The Maturity Factor formula is unchanged from the structure used across all five asset classes in this series.

For Trades Subject to a Variation Margin Agreement

| MF = (3/2) × √(MPOR / 250) |

| Same MPOR floors as the other four asset classes: 10 business days standard, 5 for client-facing trades, 20 for large or illiquid netting sets. |

For Trades Not Subject to a Variation Margin Agreement

| MF = √( min{M, 250} / 250 ) |

| M = remaining maturity in business days, floored at 10 business days |

Step 4 — The Supervisory Factor for Commodity

Table 3 to §217.132 sets out the Supervisory Factor for commodity with a notable structural feature: electricity is broken out as its own sub-category within energy, while every other commodity sub-category — including the rest of energy — shares a flat 18% factor:

| Asset Class | Category | Type | Supervisory Factor |

| Commodity | Energy | Electricity | 40% |

| Commodity | Energy | Other | 18% |

| Commodity | Metals | N/A | 18% |

| Commodity | Agricultural | N/A | 18% |

| Commodity | Other | N/A | 18% |

Electricity’s 40% Supervisory Factor is more than double the 18% applied to every other commodity sub-category — the second-highest single Supervisory Factor of any sub-category across all five asset classes in this series, behind only single-name equity (32%) it actually exceeds, reflecting the regulation’s recognition of electricity’s exceptional price volatility relative to other physical commodities.

The Supervisory Correlation Factor for commodity is a single flat 40% that applies uniformly across all four categories — energy, metals, agricultural, and other — unlike equity and credit where ρ varies between single-name and index.

Putting It Together — The ADCA Formula

| ADCA = Adjusted Notional × Supervisory Delta × Maturity Factor × Supervisory Factor |

| Worked Example 3 — Full ADCA Calculation (Crude Oil) Trade: Swap on 100,000 barrels WTI crude (from Example 1) Bank is long crude (benefits if price rises) Maturity: 9 months, not subject to a variation margin agreement Adjusted Notional (from Example 1): $7,850,000 Supervisory Delta (long the commodity): +1 Maturity Factor: M = 9 months ≈ 188 business days MF = √(min(188,250)/250) = √(188/250) = √0.752 = 0.867 Supervisory Factor (Energy, Other): 18% ADCA = 7,850,000 × 1 × 0.867 × 0.18 ADCA = $1,224,747 |

| Worked Example 4 — Same Notional, Electricity Instead of Crude Oil Identical trade terms, but referencing an electricity forward Supervisory Factor (Energy, Electricity): 40% ADCA = 7,850,000 × 1 × 0.867 × 0.40 ADCA = $2,721,660 The electricity version of this trade produces an ADCA more than double the crude oil version, purely from the Supervisory Factor difference (40% vs 18%) on identical notional and maturity. |

Figure 1: Commodity hedging set build-up — single correlation factor across all commodity types | Source: 12 CFR §217.132(c)(8)(iv), (c)(9)

Step 5 — Grouping by Commodity Type

Within a single commodity hedging set (recall: one hedging set already exists per category — energy, metal, agricultural, or other), trades are further grouped by the specific commodity type they reference. ADCAs for trades referencing the same type are summed:

| AddOn(Type_k) = Σ ADCA for all trades referencing commodity type k |

| k indexes each distinct commodity type within the category. Within the energy hedging set, for example, k might separately index crude oil, natural gas, and electricity. |

This is conceptually similar to equity and credit’s reference-entity grouping, but the terminology in the regulation specifically refers to commodity type rather than reference entity, and — as shown in Step 6 below — the aggregation formula treats all types within a category with a single shared correlation factor, rather than allowing the correlation factor itself to vary by type the way it varies between single-name and index in equity and credit.

Step 6 — Calculating the Hedging Set Amount

The commodity Hedging Set Amount formula has the same two-term systematic-plus-idiosyncratic structure as equity and credit, but with one key simplification: a single ρ = 40% applies across the entire summation, rather than a per-type ρk as in equity and credit’s per-reference-entity formula.

| HSA = [ (ρ × Σ AddOn(Typek))² + (1−ρ²) × Σ (AddOn(Typek))² ]^(1/2) |

| ρ = 40% (flat, applies to all commodity types). Summations run over all k commodity types within the hedging set category. |

The economic logic mirrors equity and credit: the first term captures the systematic component of commodity risk (broad commodity-cycle co-movement, dollar-driven commodity price correlations), and the second term captures the idiosyncratic component specific to each individual commodity type (a localised supply disruption in one specific metal, weather-driven price spikes in one specific agricultural product).

| Worked Example 5 — Hedging Set Amount Within the Energy Category Energy hedging set contains three commodity types: Type 1 (crude oil): AddOn = $1,224,747 Type 2 (natural gas): AddOn = $680,000 Type 3 (electricity): AddOn = $2,721,660 ρ = 0.40 (applies to all three types) Systematic term: ΣAddOn(Typek) = 1,224,747 + 680,000 + 2,721,660 = $4,626,407 ρ×ΣAddOn(Typek) = 0.40 × 4,626,407 = $1,850,563 Squared: (1,850,563)² ≈ 3.4246E12 Idiosyncratic term: (1-ρ²) = (1-0.16) = 0.84 Σ(AddOn(Typek))² = (1,224,747)²+(680,000)²+(2,721,660)² = 1.4996E12 + 4.6240E11 + 7.4074E12 = 9.4294E12 0.84 × 9.4294E12 = 7.9207E12 HSA = [3.4246E12 + 7.9207E12]^(1/2) = [1.1345E13]^(1/2) HSA ≈ $3,368,000 Compare to a simple sum of AddOns (1,224,747+680,000+2,721,660 = $4,626,407) — the correlation formula recognises some diversification, though less dramatically than equity or credit since the single flat ρ = 40% gives less idiosyncratic credit than equity’s 50%/80% or credit’s 50%/80% structures. |

Comparing Commodity to Equity and Credit

Having now covered all three asset classes that use the reference-entity-style grouping and correlation formula — equity, credit, and commodity — it is worth summarising the key structural differences:

| Feature | Equity | Credit | Commodity |

| Hedging set defined by | Entire netting set | Entire netting set | Per category (4 categories) |

| Grouping variable | Reference entity | Reference entity | Commodity type |

| Correlation factor (ρ) | 50% / 80% | 50% / 80% | Flat 40% |

| Supervisory Factor range | 20% – 32% | 0.38% – 6.0% | 18% – 40% |

| Duration adjustment needed? | No | Yes | No |

Commodity’s single flat correlation factor is the simplest of the three. Credit has by far the widest Supervisory Factor range, reflecting the non-linear relationship between credit quality and default risk. Equity and credit share an identical Hedging Set Amount formula structure; commodity uses a simplified version of that same structure with one shared ρ rather than a per-grouping ρ.

Special Cases Within the Commodity Asset Class

Basis and Volatility Derivative Contracts

As with interest rate, exchange rate, and equity, commodity basis derivative contracts and volatility derivative contracts each require their own separately calculated hedging set amount, using whichever formula corresponds to the primary risk factor. The applicable Supervisory Factor for a commodity basis derivative hedging set is one-half of the standard factor in Table 3; for a commodity volatility derivative hedging set, it is five times the standard factor.

Cross-Category Commodity Derivatives

A derivative contract whose risk materially depends on more than one of the recognised risk factor categories may, at the Board’s discretion, be required to be included in each appropriate hedging set rather than assigned to only one. This applies across all asset classes but is particularly relevant for commodity, where some structured products can reference baskets spanning energy and metals simultaneously.

Settlement Currency Mismatches

Commodity derivatives are frequently denominated in US dollars regardless of where the underlying physical commodity is produced or consumed (oil, for example, is conventionally priced in USD globally). Where a commodity derivative’s notional is genuinely denominated in a non-USD currency, the same currency conversion to USD that applies across all asset classes is required before the Adjusted Notional calculation.

Quick Summary

- Commodity hedging sets are defined per category — energy, metal, agricultural, or other — unlike equity and credit, which form a single hedging set per netting set regardless of how many reference entities are involved.

- Adjusted Notional for commodity uses the same simple fair-value-times-units formula as equity — no duration adjustment is required.

- The Supervisory Factor is 40% for electricity and a flat 18% for every other commodity sub-category (other energy, metals, agricultural, other).

- Supervisory option volatility is 150% for electricity and 70% for all other commodity types.

- ADCAs are grouped by commodity type (analogous to reference entity in equity and credit) before aggregation.

- The Hedging Set Amount formula uses a single flat correlation factor of 40% across all commodity types within a category — unlike equity and credit, which use different ρ values for single-name versus index.

- Electricity’s exceptionally high Supervisory Factor (40%) and option volatility (150%) reflect the well-documented extreme price volatility unique to electricity markets, driven by the inability to store electricity economically at scale.

Frequently Asked Questions

Why does commodity split into separate hedging sets per category, while equity and credit do not?

The regulation treats energy, metals, agricultural products, and other commodities as sufficiently distinct risk factors that they do not belong in the same hedging set together — crude oil prices and wheat prices are not considered to share enough common risk drivers to be aggregated within one undifferentiated commodity hedging set. Equity and credit, by contrast, are each treated as a single broad risk factor category at the hedging-set level, with the single-name/index and reference-entity distinctions handled entirely within the Hedging Set Amount formula rather than through separate hedging sets.

Why is electricity treated so differently from other energy commodities?

Electricity has fundamentally different physical and market characteristics from other energy commodities like crude oil or natural gas. It cannot be economically stored at scale, meaning supply and demand must balance in real time, which produces extreme price volatility — including periods of negative prices during oversupply and dramatic spikes during demand surges or generation shortfalls. The Supervisory Factor (40% vs 18%) and option volatility (150% vs 70%) for electricity reflect this empirically much higher volatility.

Why does commodity use a single flat correlation factor instead of varying it like equity and credit?

Equity and credit vary ρ based on a clear, binary single-name versus index distinction that has a strong economic rationale — index products are inherently more diversified and more correlated with broad systematic risk. Commodity does not have an equivalent index-versus-single-name structure in the same way; instead, the diversification question in commodity is about differentiation between distinct underlying commodity types within a category. The regulation addresses this with one flat correlation factor that applies regardless of which specific commodities are being aggregated together within the category.

How does the commodity Hedging Set Amount formula simplify compared to equity and credit?

In equity and credit, the formula sums ρk×AddOn(Refk) before squaring, where ρk can differ for each reference entity (50% for single-name, 80% for index) — requiring the correlation factor to be applied individually to each term before summation. In commodity, since ρ is the same flat 40% for every type, the formula can equivalently be written as ρ multiplied by the simple sum of all AddOns, then squared — mathematically simpler because there is only one correlation value to apply across the entire category.