Introduction

Replacement cost is the first of two building blocks inside the SA-CCR exposure calculation. In the SA-CCR formula — EAD = 1.4 × (RC + PFE) — Replacement Cost answers a specific question: if the counterparty defaulted right now, how much would it cost the bank to replace the contracts in that netting set at today’s market prices?

It is, in other words, the current exposure. Not a forecast. Not a worst-case. The actual mark-to-market loss the bank would face if it had to go into the market today and recreate every position with a new counterparty at prevailing prices.

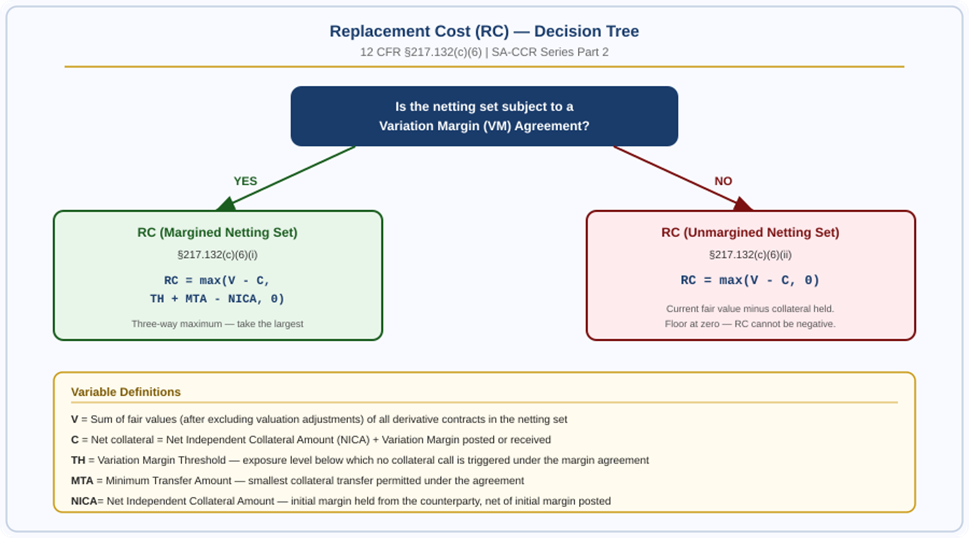

The calculation of Replacement Cost splits into two distinct paths depending on one key question: is the netting set covered by a variation margin agreement? If yes, the counterparty is posting collateral regularly to offset mark-to-market movements. If no, there is no such cushion. Each path has its own formula under 12 CFR §217.132(c)(6), and they produce meaningfully different results.

This article covers both paths in full — with worked examples, the complete haircut table, and a clear explanation of every variable. By the end, you will understand exactly how a bank moves from a portfolio of derivative contracts to a single Replacement Cost number that feeds into its capital calculation.

Figure 1: Replacement Cost decision tree — margined vs unmargined netting set | Source: 12 CFR §217.132(c)(6)

Path 1 — The Unmargined Netting Set

An unmargined netting set is a group of derivative contracts where no variation margin agreement is in place — or where one exists but the counterparty is not required to post variation margin. This is the simpler of the two cases.

The Formula

| RC = max ( V − C , 0 ) |

| Floor at zero: Replacement Cost cannot be negative. If the portfolio is out-of-the-money for the bank (V < C), the bank owes the counterparty — and faces no current credit exposure. |

Breaking Down the Variables

V — Fair Value of the Netting Set

V is the sum of the current fair values of all derivative contracts in the netting set, after excluding any valuation adjustments such as CVA. If the portfolio of contracts is worth $8 million to the bank, V = $8m. This is a mark-to-market number — it changes every day as underlying rates, prices, and credit spreads move.

C — Net Collateral Amount

C is the value of collateral the bank currently holds from the counterparty, net of any collateral the bank has posted to the counterparty. Under §217.132(c)(6)(ii), C is the sum of the net independent collateral amount and the variation margin applicable to the contracts.

Critically, C is not simply the face value of the collateral. It must be adjusted downward by supervisory haircuts — which we cover in detail in the Haircut section below — to reflect the risk that collateral values can fall.

| Worked Example 1 — Unmargined Netting Set Portfolio fair value (V): +$12,000,000 Collateral held (equity securities, after haircut): -$3,750,000 (Face value $5m × (1 − 25% haircut) = $3.75m) RC = max(12,000,000 − 3,750,000, 0) RC = max(8,250,000, 0) RC = $8,250,000 The bank’s current exposure is $8.25 million. |

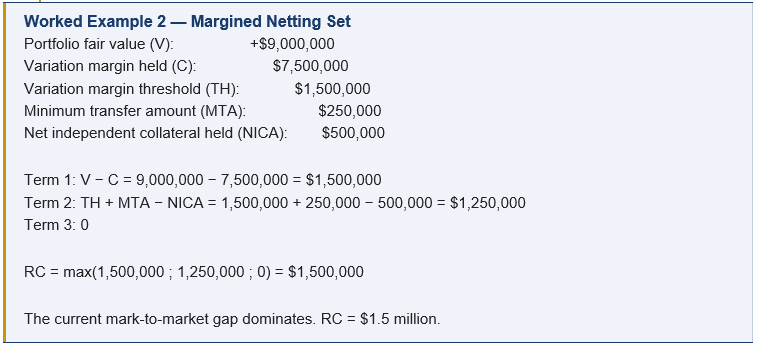

Path 2 — The Margined Netting Set

A margined netting set is covered by a variation margin (VM) agreement under which the counterparty must post VM. This introduces several additional variables — the threshold, the minimum transfer amount, and the net independent collateral amount — each of which reflects a practical feature of how margin agreements actually work.

The Formula

| RC = max ( V − C , TH + MTA − NICA , 0 ) |

| Three-way maximum: the RC is the greatest of these three quantities. The floor of zero still applies. |

Why Three Terms?

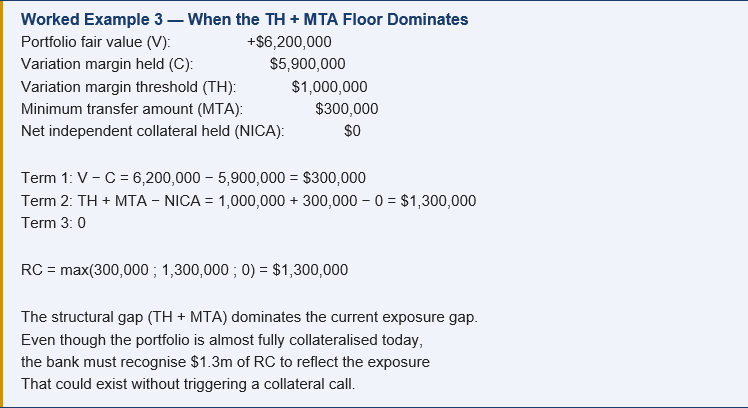

This formula reflects a practical reality: even in a perfectly functioning margin agreement, there is always a window of uncovered exposure. The counterparty does not post collateral for every fraction of a dollar of exposure. The threshold (TH) and minimum transfer amount (MTA) define exactly how large that uncovered window can be.

The regulation is precise about this. Under §217.132(c)(6)(i), Replacement Cost for a margined set is the greatest of:

- V − C: the current mark-to-market exposure net of collateral already held

- TH + MTA − NICA: the maximum exposure that could exist without triggering a collateral call

- Zero: RC cannot be negative

Understanding Each Variable

TH — Variation Margin Threshold

The threshold is the exposure level below which the counterparty is not required to post any variation margin. If the threshold is $2 million, and the portfolio’s fair value (net of existing collateral) rises to $1.9 million, no margin call occurs. Only when exposure exceeds $2 million does a call get triggered.

Thresholds exist because posting and receiving collateral every day for tiny amounts would be operationally impractical. But they create a structural gap in coverage: the bank may always have exposure up to the threshold level that is not collateralised.

MTA — Minimum Transfer Amount

Even when exposure exceeds the threshold, the minimum transfer amount is the smallest collateral transfer that can be made. If the MTA is $500,000, and exposure rises by $300,000 above the threshold, no transfer occurs because the required amount is below the MTA.

Like the threshold, the MTA creates a gap — but a smaller one. Together, TH + MTA represents the maximum uncollateralised exposure that the margin agreement structurally permits.

NICA — Net Independent Collateral Amount

NICA is the initial margin that the bank holds from the counterparty, net of any initial margin the bank has posted to that same counterparty. Initial margin is posted at the inception of a trade as a forward-looking buffer. It is not returned daily like variation margin — it sits as a permanent cushion.

NICA directly reduces the TH + MTA floor. If the bank holds $3 million of initial margin (NICA = $3m) and the sum of TH + MTA is $2.5 million, the floor becomes $2.5m − $3m = −$0.5m, which is then dominated by the zero floor. In effect, sufficient initial margin can eliminate the structural exposure gap entirely.

“A Board-regulated institution may recognize the credit risk mitigation benefits of financial collateral that secures an eligible margin loan, repo-style transaction, or single-product netting set of such transactions by factoring the collateral into its LGD estimates for the exposure.”

Collateral Haircuts — What They Are and Why They Matter

Collateral is not worth its face value for regulatory purposes. A counterparty posting $10 million of equities as collateral does not give the bank $10 million of protection — because equity prices can fall sharply, especially during a market stress event, which is exactly when the counterparty is most likely to default.

Supervisory haircuts address this directly. They are downward adjustments applied to the face value of collateral before it is counted as C in the RC formula. The regulation provides a standard table of haircuts (Table 1 to §217.132) that all Board-regulated institutions must use unless they have received prior approval to use their own internal estimates.

The haircut formula is:

| C (adjusted) = Collateral Face Value × (1 − Hs) |

| Where Hs is the applicable supervisory haircut from Table 1. The adjusted value is what enters the RC formula as C. |

The Standard Supervisory Haircut Table

The following table is drawn directly from Table 1 to §217.132 and covers the full range of eligible collateral types:

| Instrument | Residual Maturity | Haircut (Hs) |

| Sovereign (0% RW) | <= 1 year | 0.5% |

| Sovereign (0% RW) | 1 to 5 years | 2.0% |

| Sovereign (0% RW) | > 5 years | 4.0% |

| Sovereign (20%/50% RW) | <= 1 year | 1.0% |

| Non-sovereign (20% RW) | <= 1 year | 1.0% |

| Non-sovereign (50% RW) | <= 1 year | 2.0% |

| Non-sovereign (100% RW) | Any | 4–16% |

| Investment grade securitisations | Any | 4–24% |

| Main index equities / Gold | N/A | 15% |

| Other publicly traded equities | N/A | 25% |

| Cash collateral | N/A | 0% |

| FX mismatch (Hfx) | N/A | 8% |

| Other / non-financial collateral | N/A | 25% |

Source: Table 1 to §217.132 (12 CFR Part 217). Haircuts based on a 10 business-day holding period.

The 8% FX Haircut

A separate haircut applies when there is a currency mismatch between the collateral and the settlement currency of the contract. If a netting set is settled in US dollars but the counterparty posts euro-denominated bonds as collateral, an additional 8% FX haircut (Hfx) is applied to that position.

This reflects the risk that exchange rate movements could reduce the effective value of the collateral before it can be liquidated and converted.

“For currency mismatches, a Board-regulated institution must use a haircut for foreign exchange rate volatility (Hfx) of 8 percent, as adjusted in certain circumstances as provided in paragraphs (b)(2)(ii)(A)(3) and (4) of this section.”

Adjusted Holding Periods

The standard haircuts are calibrated to a 10-business-day holding period for eligible margin loans and derivative contracts, and a 5-business-day holding period for repo-style transactions. When the actual holding period differs from these standards, haircuts must be scaled using the square root of time formula:

| HA = HS × √(TM / TS) |

| HA = adjusted haircut | HS = standard supervisory haircut | TM = actual holding period | TS = standard holding period (10 or 5 days) |

For example, if a netting set has more than 5,000 trades at any point in a quarter, the minimum holding period increases to 20 business days for the following quarter. This longer period reflects the greater difficulty of closing out and re-hedging a very large book quickly.

The regulation is also explicit about when holding periods must be extended beyond the standard:

- Netting sets with more than 5,000 derivative contracts at any point in a quarter: minimum 20-business-day holding period for the following quarter

- Netting sets containing illiquid collateral or derivatives that cannot be easily replaced: minimum 20-business-day holding period

- Netting sets where more than two margin disputes lasting longer than the holding period occurred in the previous two quarters: holding period must be at least twice the standard minimum

Using Own Internal Haircut Estimates

With prior written approval from the Board, a bank may use its own internally estimated haircuts rather than the standard supervisory table. This is permitted under §217.132(b)(2)(iii) and requires the bank to meet strict quantitative standards:

- Use a 99th percentile one-tailed confidence interval

- Calibrate to a continuous 12-month period of historical data that includes a period of significant financial stress

- Update data sets and recalculate haircuts at least quarterly

- Obtain prior Board approval and notify the Board of any material changes to the methodology

Internal haircut models allow banks to be more precise — particularly for unusual or bespoke collateral where the standard table’s catch-all 25% haircut may be either too conservative or insufficiently so. But the approval bar is high and the ongoing obligations are significant.

“A Board-regulated institution must update its data sets and calculate haircuts no less frequently than quarterly and must also reassess data sets and haircuts whenever market prices change materially.”

Collateral Recognition — Three Available Methodologies

For eligible margin loans and repo-style transactions, the regulation provides three distinct methodologies for recognising the risk-reduction benefit of collateral. Under §217.132(a), a bank may use:

1. The Collateral Haircut Approach

This is the standard approach described throughout this article. Collateral is valued at its face amount adjusted downward by the applicable supervisory haircut. The adjusted value of C is then netted against V to determine RC. Simple, transparent, and based on a standard table — no modelling required beyond applying the published haircuts.

The EAD equation under this approach for eligible margin loans and repo-style transactions is:

| EAD = max{ 0, [ΣE − ΣC] + Σ(Es × Hs) + Σ(Efx × Hfx) } |

| Where ΣE = total exposure value, ΣC = total collateral value, Es = net position in each security, Hs = applicable haircut, Efx = FX-mismatched net position, Hfx = 8% FX haircut |

2. The Simple VaR Methodology

With prior Board approval, a bank may use an internal VaR model to estimate EAD for single-product netting sets of repo-style transactions and eligible margin loans. The formula is:

| EAD = max{ 0, [ΣE − ΣC] + PFE } |

| Where PFE is the 99th percentile one-tailed confidence interval for an increase in (ΣE − ΣC) over the applicable holding period |

The VaR model must be validated through a rigorous backtesting regime and must use a minimum one-year historical observation period. This approach is more risk-sensitive than the haircut approach but requires significantly more infrastructure and model oversight.

3. The Internal Models Methodology (IMM)

The most sophisticated option — covered in full in Part 5 of this series. The IMM allows banks to model EAD using their own expected exposure models across the full remaining life of the netting set. It requires the most extensive Board approval process and ongoing validation obligations, but can produce materially lower capital requirements for well-collateralised books.

A bank may use any combination of these three methodologies but must apply the same methodology consistently to all transactions in the same category. It cannot, for example, use the haircut approach for some repo trades and the VaR approach for others within the same category.

Special Case — Multiple Netting Sets Under One Margin Agreement

A practical complication arises when multiple netting sets are subject to a single variation margin agreement. This is common in large bilateral relationships where a bank and counterparty use a single CSA to govern margin across many separate trade portfolios.

In this case, §217.132(c)(10)(i) requires the bank to calculate a single Replacement Cost across all the netting sets covered by that agreement:

| RC = max{ΣNS max{VNS; 0} − max{CMA; 0}; 0} + max{ΣNS min{VNS; 0} − min{CMA; 0}; 0} |

| VNS = fair value of each netting set NS | CMA = total collateral under the single margin agreement |

This formula separately handles the netting sets with positive fair value and those with negative fair value, and then nets total collateral against the aggregate. The structure prevents a bank from double-counting collateral benefits by allocating all of one pool of collateral to the most favourable netting set.

Quick Summary

- Replacement Cost measures the current cost of replacing a defaulted counterparty’s contracts at today’s market prices.

- For unmargined netting sets: RC = max(V − C, 0). Simple net of fair value minus haircut-adjusted collateral.

- For margined netting sets: RC = max(V − C, TH + MTA − NICA, 0). The three-way maximum captures both the current gap and the structural exposure gap created by the threshold and minimum transfer amount.

- Collateral must be haircut before it is counted. Standard supervisory haircuts range from 0% (cash) to 25% (equities and non-standard collateral). An additional 8% applies for currency mismatches.

- Holding periods can extend to 20 business days for large netting sets, illiquid collateral, or netting sets with repeated margin disputes.

- Three methodologies are available for collateral recognition: the standard haircut approach, the simple VaR methodology (Board approval required), and the internal models methodology (Board approval required).

- Multiple netting sets under a single margin agreement require a consolidated RC calculation that prevents double-counting of collateral.

Frequently Asked Questions

What is Replacement Cost in SA-CCR?

Replacement Cost is the current exposure component of the SA-CCR EAD calculation. It answers the question: if the counterparty defaulted today, how much would it cost the bank to recreate those contracts in the market at current prices? It is calculated as the fair value of the netting set minus the value of collateral held, with a floor of zero.

What is the difference between a margined and unmargined netting set?

A margined netting set is covered by a variation margin agreement under which the counterparty is required to post collateral as market values change. An unmargined set has no such agreement. The RC formula is simpler for unmargined sets (RC = max(V-C, 0)) but the margined formula introduces a structural floor (TH + MTA – NICA) that captures the residual exposure that margin agreements cannot fully eliminate.

Why can Replacement Cost not be negative?

If the portfolio has negative fair value to the bank (meaning the bank owes money to the counterparty), the bank faces no current credit exposure on that netting set. The counterparty would benefit from the bank’s default, not be harmed by it. RC is floored at zero to reflect this: credit exposure only exists when the counterparty owes money to the bank.

What is NICA and why does it reduce the RC floor?

NICA (Net Independent Collateral Amount) is the initial margin held from the counterparty, net of initial margin posted. It reduces the TH + MTA floor because it provides a forward-looking buffer that already covers part of the structural exposure gap. If NICA exceeds TH + MTA, the floor is effectively zero — the initial margin is sufficient to cover any gap that the margin agreement’s threshold and minimum transfer amount would otherwise leave uncovered.

Why do haircuts vary so widely — from 0% for cash to 25% for equities?

Haircuts reflect the liquidity and price volatility of the collateral. Cash has no price risk — $1 of cash is always worth $1 (in the same currency). Short-dated government bonds from highly rated sovereigns have minimal price risk over a 10-day holding period. Equities can fall 20–30% in a matter of days during a market crisis — exactly when a counterparty default is most likely. The 25% haircut for equities reflects this worst-case scenario risk.

Can a bank use its own haircut estimates instead of the standard table?

Yes, with prior written approval from the Board of Governors. Own-estimate haircuts must be based on a 99th percentile one-tailed confidence interval, calibrated to a stress period, and updated at least quarterly. The bank must also have policies and procedures for determining the stress period and must notify the Board of any material changes.