Introduction

The interest rate asset class is, in almost every derivatives portfolio, the largest single contributor to a bank’s PFE add-on. Interest rate swaps, caps, floors, and swaptions make up the vast majority of OTC derivative notional outstanding globally — and SA-CCR dedicates a distinctly more granular set of rules to this asset class than to any other.

This article picks up exactly where Part 1 left off: the Adjusted Derivative Contract Amount (ADCA) and Hedging Set Amount, applied specifically and exhaustively to interest rate derivatives. We will not touch the PFE Multiplier or final risk-weighted asset calculation here — those are covered in a later article in this series once all five asset classes have been built up individually.

By the end of this article, you will be able to take a real interest rate swap book, calculate the ADCA for each trade, assign each trade to the correct maturity time bucket, and aggregate those buckets into a single Hedging Set Amount exactly as a bank’s regulatory reporting team would.

Why Interest Rate Trades Are Treated Differently

Unlike exchange rate or commodity derivatives, where a single trade’s add-on stands largely on its own, interest rate trades within the same currency are explicitly correlated with each other across time. A 2-year swap and an 8-year swap in the same currency do not move independently — they are both driven by the same underlying yield curve.

To capture this, the regulation requires interest rate trades to be split into three maturity time buckets based on each contract’s end date, and then combined using a formula that accounts for the partial correlation between buckets. This is the single most distinctive feature of the interest rate asset class methodology.

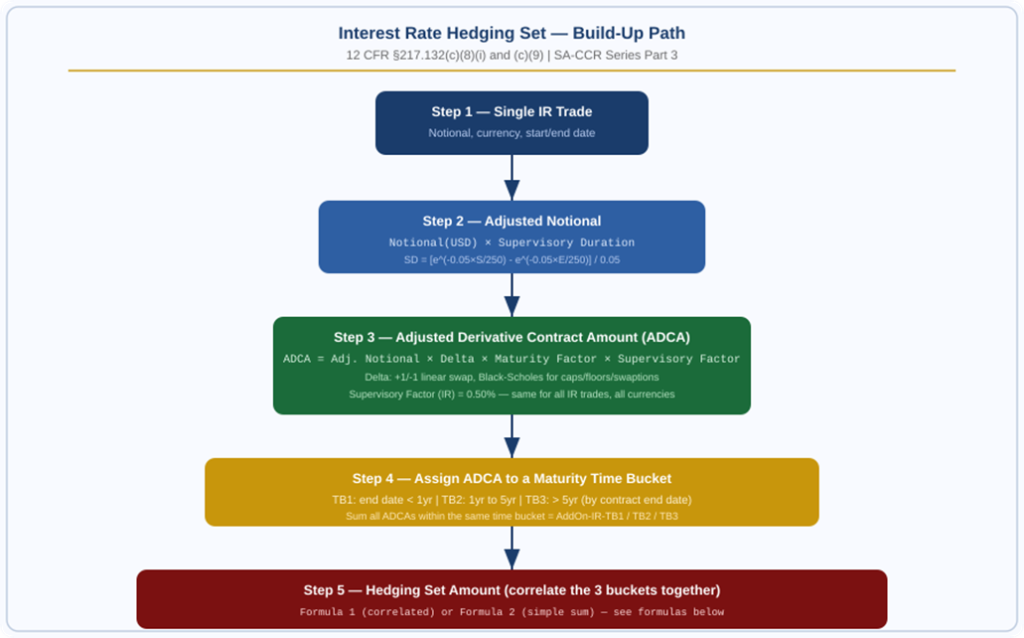

Step 1 — Calculate the Adjusted Notional

Every interest rate derivative contract begins with a notional amount — the reference amount on which payments are calculated. Before this notional can be used in the ADCA formula, it must be converted into an Adjusted Notional that reflects the time value of the contract’s remaining cash flows.

The Supervisory Duration Formula

| SD = [ e^(−0.05 × S/250) − e^(−0.05 × E/250) ] / 0.05 |

| S = business days from today until the contract’s start date (0 if already started) | E = business days from today until the contract’s end date | Floor: SD ≥ 0.04 |

The Adjusted Notional is then:

| Adjusted Notional = Notional (in USD) × Supervisory Duration |

| Notional must be converted to US dollars using the exchange rate on the calculation date if denominated in another currency. |

| Worked Example 1 — Supervisory Duration for a 5-Year Swap Trade: $50,000,000 notional interest rate swap Start date: today (S = 0 business days) End date: 5 years from today (E = 1,250 business days, approx.) SD = [e^(-0.05 × 0/250) – e^(-0.05 × 1250/250)] / 0.05 SD = [e^0 – e^(-0.25)] / 0.05 SD = [1.0000 – 0.7788] / 0.05 SD = 0.2212 / 0.05 SD = 4.424 Adjusted Notional = $50,000,000 × 4.424 = $221,200,000 |

Notice how the Adjusted Notional is considerably larger than the face notional. This reflects the cumulative interest rate sensitivity of a swap over its full remaining life — a longer-dated swap has more total cash flow exposure to rate movements than its notional alone suggests.

Special Notional Rules

Two specific situations require adjustment to the notional before the Supervisory Duration is applied:

Variable Notional Swaps

For an amortising or accreting swap where the notional changes over the life of the trade, the notional used is the time-weighted average of the contractual notional amounts over the remaining life of the swap — not simply the current or initial notional.

Leveraged Swaps

For a leveraged swap, where the notional of all legs is divided by a factor and all rates are multiplied by the same factor, the notional amount used must be the notional of an equivalent unleveraged swap. A bank cannot reduce its regulatory notional simply by structuring a trade with embedded leverage.

Step 2 — Determine the Supervisory Delta

The Supervisory Delta adjusts the Adjusted Notional for the direction and, for options, the convexity of the position.

For Linear Instruments (Swaps, FRAs)

| Delta = +1 (if value rises when the risk factor rises) or −1 (if value falls) |

| A pay-fixed swap that gains value when rates rise has delta +1. A receive-fixed swap has delta -1. |

For Options (Caps, Floors, Swaptions)

Interest rate options use the full Black-Scholes-style delta formula from Table 2 to §217.132. For a bought call option (such as a long cap):

| Delta = Φ( [ln(P/K) + 0.5σ²T/250] / (σ√(T/250)) ) |

| Φ = standard normal CDF | P = current fair value of the underlying rate | K = strike | T = business days to exercise | σ = supervisory option volatility (50% for IR) |

For interest rate options on currencies with negative rates, a shift parameter λ is added to both P and K before applying the formula, calculated as λ = max{−L + 0.1%, 0} where L is the lowest value of P or K across all IR options in that currency. This prevents the formula from breaking down when rates go negative.

Step 3 — Calculate the Maturity Factor

The Maturity Factor scales the ADCA based on how long the position remains open and how frequently it is margined. Two formulas apply depending on whether the trade is subject to a variation margin agreement.

For Trades Subject to a Variation Margin Agreement

| MF = (3/2) × √(MPOR / 250) |

| MPOR (Margin Period of Risk) = time from last collateral exchange to close-out and re-hedging. Minimum 10 business days (5 for client-facing trades), plus periodicity of re-margining minus 1 day. |

For Trades Not Subject to a Variation Margin Agreement

| MF = √( min{M, 250} / 250 ) |

| M = remaining maturity in business days, floored at 10 business days |

The MPOR floor extends to 20 business days when the netting set contains more than 5,000 derivative contracts that are not cleared transactions, contains illiquid collateral, or has experienced more than two margin disputes lasting longer than the MPOR in the previous two quarters.

Step 4 — The Supervisory Factor for Interest Rate

Unlike most other asset classes, the interest rate Supervisory Factor does not vary by tenor, currency, or credit quality. It is a single flat number:

| Supervisory Factor (Interest Rate) = 0.50% |

| This single factor applies uniformly to every interest rate derivative contract, regardless of currency or counterparty. |

This simplicity is intentional — the regulation captures the time-dimension of interest rate risk through the Supervisory Duration and the three-bucket structure described below, not through a varying supervisory factor.

Putting It Together — The ADCA Formula

| ADCA = Adjusted Notional × Supervisory Delta × Maturity Factor × Supervisory Factor |

| Worked Example 2 — Full ADCA Calculation Trade: $50,000,000 pay-fixed interest rate swap, 5-year maturity Subject to a daily variation margin agreement Adjusted Notional (from Example 1): $221,200,000 Supervisory Delta (pay-fixed, linear): +1 MPOR: 10 business days (standard, daily VM) Maturity Factor = 1.5 × √(10/250) = 1.5 × 0.2 = 0.300 Supervisory Factor (Interest Rate): 0.50% ADCA = 221,200,000 × 1 × 0.300 × 0.005 ADCA = $331,800 |

Figure 1: Interest rate hedging set build-up — from single trade to Hedging Set Amount | Source: 12 CFR §217.132(c)(8)(i), (c)(9)

Step 5 — Assigning Trades to Maturity Time Buckets

Once the ADCA is calculated for every individual interest rate trade in a hedging set, each trade must be assigned to one of three maturity time buckets based on its end date — the same end date used in the Supervisory Duration calculation.

| Time Bucket | End Date Range | Label |

| TB1 | Less than 1 year from today | AddOn-IR-TB1 |

| TB2 | 1 year to 5 years from today | AddOn-IR-TB2 |

| TB3 | Greater than 5 years from today | AddOn-IR-TB3 |

Within each time bucket, all ADCAs for trades referencing the same hedging set are simply summed. A hedging set, recall from Part 1, is defined for interest rate derivatives as all such contracts within a netting set that reference the same reference currency. So a bank with USD swaps and EUR swaps against the same counterparty has two separate interest rate hedging sets — one per currency — each independently split into TB1, TB2, and TB3.

Step 6 — Calculating the Hedging Set Amount

With AddOn-IR-TB1, TB2, and TB3 calculated, the regulation offers a choice between two formulas to combine them into the final Hedging Set Amount for that currency.

Formula 1 — The Correlated Formula

This formula recognises that adjacent time buckets are more correlated with each other than distant ones — a 3-year position and a 4-year position move together more closely than a 1-year position and a 9-year position.

| Hedging Set Amount = [ (TB1)² + (TB2)² + (TB3)² + 1.4×TB1×TB2 + 1.4×TB2×TB3 + 0.6×TB1×TB3 ]^(1/2) |

| The cross-terms (1.4 for adjacent buckets, 0.6 for the most distant pair) build in partial correlation between maturity buckets. |

Formula 2 — The Simple Sum

A more conservative alternative that simply adds the absolute values of the three buckets, without recognising any diversification benefit between them:

| Hedging Set Amount = |TB1| + |TB2| + |TB3| |

| Always produces a result equal to or greater than Formula 1. Banks may choose either formula but should apply it consistently. |

| Worked Example 3 — Full Hedging Set Amount (USD Hedging Set) Assume the following ADCAs after summing all trades in each bucket: AddOn-IR-TB1 (trades maturing < 1yr): $180,000 AddOn-IR-TB2 (trades maturing 1-5yr): $331,800 AddOn-IR-TB3 (trades maturing > 5yr): $410,000 Using Formula 1 (correlated): HSA = [ (180,000)² + (331,800)² + (410,000)² + 1.4×180,000×331,800 + 1.4×331,800×410,000 + 0.6×180,000×410,000 ]^(1/2) HSA = [ 3.24E10 + 1.10E11 + 1.681E11 + 8.365E10 + 1.905E11 + 4.428E10 ]^(1/2) HSA = [6.317E11]^(1/2) HSA = $794,800 (approx.) Using Formula 2 (simple sum) for comparison: HSA = 180,000 + 331,800 + 410,000 = $921,800 Formula 1 produces a lower figure because it recognises that the three time buckets are not perfectly correlated with each other. |

This Hedging Set Amount for the USD interest rate hedging set then becomes one input into the Aggregated Amount (the sum across all hedging sets and asset classes), which in turn feeds the PFE Multiplier and final PFE calculation — covered once all five asset classes have been built up individually later in this series.

Special Cases Within the Interest Rate Asset Class

Basis Derivative Contracts

A basis swap — for example, one that exchanges a 3-month SOFR-based floating rate for a 6-month SOFR-based floating rate — references two different risk factors within the same currency. The regulation requires basis derivative hedging sets to be calculated separately from standard single-rate hedging sets, using whichever of the standard formulas corresponds to the primary risk factor, but applying a Supervisory Factor equal to one-half of the standard 0.50% — that is, 0.25%.

Volatility Derivative Contracts

An interest rate volatility derivative — such as a swaption straddle traded purely for volatility exposure — is treated with a Supervisory Factor equal to five times the standard factor, reflecting the materially higher sensitivity of volatility products to market movements. For IR volatility products, this means a Supervisory Factor of 2.50% rather than 0.50%.

Currency Conversion

All interest rate notional amounts must be converted to US dollars using the exchange rate on the date of calculation before the Adjusted Notional formula is applied. A bank with swaps in ten different currencies converts every single notional to USD before bucket assignment — bucket assignment and aggregation always happen in a single common currency.

Quick Summary

- Interest rate trades require a Supervisory Duration calculation to convert notional into Adjusted Notional — reflecting the cumulative rate sensitivity across the trade’s remaining life.

- ADCA = Adjusted Notional × Supervisory Delta × Maturity Factor × Supervisory Factor. The IR Supervisory Factor is a flat 0.50% regardless of tenor or currency.

- Each interest rate hedging set is defined per reference currency — USD swaps and EUR swaps with the same counterparty form two separate hedging sets.

- Within each hedging set, trades are split into three time buckets by end date: less than 1 year, 1 to 5 years, and more than 5 years.

- ADCAs within the same time bucket are summed to produce AddOn-IR-TB1, TB2, and TB3.

- The three buckets are combined into the Hedging Set Amount using either the correlated Formula 1 (recognises partial diversification) or the conservative Formula 2 (simple sum, no diversification credit).

- Basis derivatives use half the standard Supervisory Factor (0.25%); volatility derivatives use five times the standard factor (2.50%).

Frequently Asked Questions

Why does the interest rate asset class use only one Supervisory Factor for all tenors?

The regulation captures the time dimension of interest rate risk through the Supervisory Duration calculation and the three-bucket structure, rather than through a tenor-varying Supervisory Factor. A flat 0.50% factor combined with duration-adjusted notional and bucket-level correlation achieves the same risk sensitivity with a simpler factor table.

What is a hedging set for interest rate derivatives?

A hedging set for interest rate derivatives is all such contracts within a single netting set that reference the same reference currency. A bank with USD, EUR, and GBP interest rate swaps against one counterparty has three separate interest rate hedging sets, each calculated independently with its own three time buckets.

Why does Formula 1 produce a lower Hedging Set Amount than Formula 2?

Formula 1 recognises that interest rate exposures across different maturity buckets are not perfectly correlated — a position maturing in 2 years and one maturing in 8 years do not move in lockstep. The cross-terms in Formula 1 (with coefficients 1.4 and 0.6) give partial diversification credit for this imperfect correlation. Formula 2 assumes perfect correlation between all buckets, which is more conservative and always produces an equal or higher result.

How does a variable notional swap affect the Adjusted Notional calculation?

For swaps where the notional changes over time (amortising or accreting structures), the notional used in the Adjusted Notional calculation is the time-weighted average of the contractual notional amounts over the remaining life of the swap — not the current balance or the initial notional. This prevents distortion from structures where notional steps down sharply early or late in the trade’s life.

What happens to a leveraged interest rate swap under SA-CCR?

For a leveraged swap — where notional on all legs is divided by a factor and rates are multiplied by the same factor — the bank must use the notional of an equivalent unleveraged swap, not the reduced notional of the leveraged structure. This prevents banks from artificially lowering their regulatory exposure through embedded leverage.

Pingback: SA-CCR: PFE Multiplier and Exposure at Default